Africa: Africa Economic Sector Report

2013/10/13

Africa’s economy continues to show a high degree of resilience against global economic turbulences. However, the growth momentum has eased in countries with strong links to global markets and also in those where political and social tensions have increased. With a gradual recovery of the global economy, the continent’s average growth of gross domestic product (GDP) is likely to amount to 4.8% in 2013 and 5.3% in 2014. In 2012 Africa’s growth was higher at 6.6%. But this was due to the rebound of oil production in Libya. Excluding Libya, Africa’s growth was 4.2% in 2012 and is projected to accelerate to 4.5% and 5.2% in 2013 and 2014 respectively (Figure 1.1).

Resource-rich countries continue to benefit from relatively high commodity prices although easing of global demand has reduced price levels. Good harvests have boosted agricultural production in many countries and also helped to mitigate adverse effects of high international food prices on consumers. Africa’s oil exports increased significantly as Libya resumed production.

The outlook is subject to risks due to the fragile international environment and country-specific problems. Two years after the Arab revolutions, political and social tensions continue in Egypt, Libya and Tunisia. While output is gradually recovering in Egypt and Tunisia, and in Libya oil production is close to pre-revolution level, unemployment remains high in the region and political transition is slow and contentious. Some countries in northern and western Africa have also been adversely affected by the political and military conflict in Mali. In South Africa, growth was dampened by the global slowdown and labour unrest.

Figure 1.01 Africa´s Economic Growth (%)

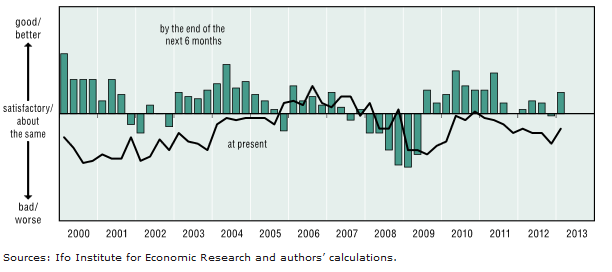

The weakness of the international environment also constrained African economies although short-term prospects appear favourable. The assessment of the economic situation by African participants in an international poll has deteriorated during 2011 and 2012. However, in the first quarter of 2013, for the first time since the end of 2010, both the assessment of the current situation and the prospects for the next six months have improved (Figure 1.2).

Figure 1.02 Africa Assessment of current Economic Situation and Expectations for the next six months

North African nations – like several other nations, which depend on European markets and have relatively high shares of total exports in GDP – are particularly exposed to the weakness of the European economy. In 2011, exporters in Tunisia, Libya, Botswana, Cape Verde and the Seychelles shipped around 70% or additional of total exports to the European Union. In Algeria, Morocco, Cameroon, Ghana, Mauritius, Mozambique and Sierra Leone, export shares to Europe amounted to between 50% and 60%. In a lot of other African nations, Europe remains the majority significant export destination despite its declining share. South Africa, whose major trading partner is the European Union, was affected by the crisis in the euro area. The volume of merchandise exports to the euro area declined sharply in the initial half of 2012. While this trade had provided a positive contribution of 0.2 % points to GDP increase in the initial half of 2011, its increase contribution in the corresponding period in 2012 was -0.6 % points; this contraction explains a good part of South Africa’s poor increase performance during this period (OECD, 2012).

In several other nations, however, China has become the majority significant export market, notably in the Democratic Republic of the Congo (DRC), Congo Rep., Sudan, Angola, Mauritania and Zambia, while the United States is the majority significant export destination for Chad and Lesotho. In Guinea-Bissau, the bulk of exports (90%) go to India.

The detailed macroeconomic estimate for Africa and its regional groupings is presented in tables 1.4a and 1.4b at the end of this chapter.

The recovery of the world economy in 2010 from the deep recession of 2009 was followed by additional moderate increase in both 2011 and 2012. The major reasons for the ongoing weakness of the world economy were the deepening crisis in the euro area, sluggish increase in other major advanced economies, notably the United States and Japan, and additional subdued increase in emerging nations such as China, India and Brazil. The permanent quantitative easing measures in the United States, Europe and Japan demonstrate how difficult it is to regain sustained increase next the financial crisis. But the risk that the world economy could fall into an extra recession has become smaller. Indeed leading economic indicators point to some development. However, there is growing concern that excessive liquidity created by stimulus measures in advanced nations could lead to new bubbles in investment markets and a fall of exchange rates below their market-based levels. This could in turn trigger competitive devaluations and new trade protectionism. The assumption of this African Economic Outlook is that such risks can be avoided and the world increase and world trade will accelerate gradually during the course of 2013/14. Our estimate for Africa assumes that world output increase will remain modest in 2013 at around 3.5% (next 2.9% in 2012) and accelerate to above 4% in 2014. World trade volume increase is projected to recover gradually from around 3% in 2012 to 4%-5% in 2013 and 6%-7% in 2014. However, these projections are lower than pre-crisis levels. From 2004 to 2007 annual increase of world output and world trade had been around 5% and around 9% respectively. The gradual recovery of world trade should benefit Africa’s exporters.

The euro area fell into recession in 2012 with GDP declining by 0.4%. The preceding two-year recovery period was short-lived and tepid (with GDP rising by 1.9% in 2010 and 1.5% in 2011 next the decline by 4.3% in 2009). GDP is expected to stagnate in 2013 or decline slightly and positive increase of 1%-1.5% is only expected in 2014. Only again, six years next the downturn has started, will GDP have regained its 2008 level. The euro area continues to struggle with weak confidence due to the ongoing sovereign deficit and banking crisis in several nations. This and the fiscal restraint are reducing domestic request while weak world trade depresses export request. The weak accumulation request makes the task of reducing fiscal deficits additional difficult. High-deficit economies are as well trying to regain increase by restoring competitiveness through lower wages (i.e. internal devaluation). While this should help increase in the longer term it reduces domestic request in the short term. Within the euro area Greece suffers the deepest and longest recession. By the end of 2013 its GDP will be additional than 25% below the level in 2007. The crisis in Greece has as well affected the banking system in Cyprus, pushing the country to the brink of bankruptcy. Part the nations which have been most seriously hit by the deficit crisis, Italy, Spain and Portugal were as well in recession in 2012. The recession in these nations is likely to continue in 2013. However, in Ireland, which was as well in crisis, the emergence from recession was faster and is presently achieving moderate increase. In Germany, GDP increased in 2012 by close to 1% while in France and in the United Kingdom GDP stagnated or declined marginally. The period of low increase is projected to continue in these nations in the initial half of 2013 with some acceleration in the second half of 2013 and in 2014.

The US economy has gradually recovered in 2012 driven mainly by private consumption and the turnaround in the housing market. Increase was, however, restrained by various temporary factors such as losses in agricultural production due to the drought and disruptions caused by Hurricane Sandy. The poor export performance and, towards the end of 2012, the risk of a large fiscal squeeze (the so-called fiscal cliff) dampened business confidence. While the major part of the fiscal cliff has been averted by a compromise between the Democrats and the Republicans, the remaining fiscal drag remains substantial, as temporary stimulus measures expired at the beginning of March 2013. Further compromises between the political parties are needed to put fiscal policy on a sustained medium-term consolidation path without unduly restraining accumulation request in the short term. It is expected that the recovery will remain

sluggish with GDP growing by around 2%-2.5% in 2013 and 2.5%-2.75% in 2014. The Federal Reserve continues to boost the economy by keeping its policy interest rate at 0%-0.25% and to increase liquidity by buying bonds. The Fed stated that it would continue these policies until the labour market improves substantially.

In Japan, accumulation request was boosted in the initial half of 2012 by reconstruction spending in response to the great earthquake and tsunami in March 2011. However, next reconstruction spending waned and world trade weakened the recovery stalled. Increase of GDP is projected to decline to around 1% in both 2013 and 2014 from about 2% in 2012. The Bank of Japan is expected to continue with expansionary policy to boost economic increase.

In China, increase has slowed down in 2012 to below 8%, from 9.3% in 2011 and 10.4% in 2010. The deceleration was mainly due to a weakening of exports and of domestic request as the government took measures to cool inflationary pressures. Nonetheless, at current increase rates, China’s economy remains robust, parrying off before fears of a hard landing of the Chinese economy. While international forecasters are expecting for 2013 increase of 8%-8.5%, China’s government in March 2013 set a lower increase target at 7.5%, unchanged from 2012. In next, the request pattern is expected to gradually shift towards consumption and services rather than commodity-intensive production. This could reduce world request for commodities, thereby adversely affecting African commodity exporters. Similarly, with rising domestic wage pressures, Chinese firms could look for additional investment in manufacturing sectors abroad. This could as well help African nations to diversify their economies.

India’s increase declined in 2012 to around 5% from 6.9% in 2011 and 9.6% in 2010. The decline was attributed to a combination of weakening of world trade and domestic uncertainties. Weaker domestic request and the depreciation of the exchange rate reduced imports and lowered the current account deficit. However, high inflation and the widening of the fiscal deficit limit the room for expansionary monetary and fiscal policies. It is expected that higher agricultural production together with positive effects of recent structural policies and improved external conditions could lead to higher increase of about 6.5% to 7% in 2013/14.

Latin America’s increase slowed in 2012 to around 3%, next 4.3% in 2011 and 6% in 2010. The slowdown was caused by weaker export markets, inclunding in China, and by country specific factors. The average rate of increase in Latin America is expected to gradually recover to 3.5% in 2013 and 4% in 2014 as world trade recovers and domestic weaknesses subside. In Brazil, the region’s major economy, increase contracted further in 2012 to around 1%, down from 2.7% in 2011 and 7.5% in 2010. The economy continued to suffer from domestic policy uncertainties, weak world conditions and a loss of competitiveness as capital inflows had led to an overvalued exchange rate. It is expected that strong monetary and fiscal stimulus coupled with supply-side reforms will gradually lift increase to 3.5% to 4% in 2013 and 2014.

- Africa News

-

- ABIDJAN: Microfinance lenders gaining ground in Côte d’Ivoire

- TUNISIA: Tunisia harvests growth in agriculture sector

- DJIBOUTI CITY: Djibouti’s tourism ambitions garner overseas support

- BOTSWANA: Tripartite Free Trade Area plods along slowly in Africa

- MAPUTO CITY: Shaken but not stirred: Mozambique's banks look forward with optimism

- NAMIBIA: Namibia, SA mourns anti-apartheid icon

- Trending Articles

-

- LIBYA: Libya unity forces take control of Tripoli airport

- PAPUA NEW GUINEA: Papua New Guinea taps renewables and gas to satisfy growing energy demand

- BRUNEI : The next chapter for the Trans-Pacific Partnership

- CHINA: Hong Kong SAR, Australia announce official launch of FTA negotiation

- JAPAN: Retirement Age Should Be Raised To 70, Says World Economic Forum

- BULGARIA: Bulgarian commissioner fields easy questions at MEP hearing