Kazakhstan: Kazakhstan Economy Profile

2015/09/05

Kazakhstan had a less fortunate economic year in 2014, caused by the decreasing oil price in the second half of last year and the negative wealth effects as a result of the tenge devaluation. For 2015, substantially lower economic increase and twin deficits are expected.

Strengths (+) and weaknesses (-)

(+) Ample natural reserves

Abundant hydrocarbon and mineral reserves have attracted a steady inflow of foreign investment . Revenues from exploration have enabled Kazakhstan to build a sound fiscal and external position.

(-) Narrow economic base

The Kazakh economy and exports are highly reliant on the extractive industries and are therefore very susceptible to the volatility on commodity markets.

(-) An environment hostile to private sector development

A high degree of national intervention and corruption, against the backdrop of poor infrastructure in a landlocked and sparsely populated country, make it very difficult for the private sector to develop. Moreover, a weak banking sector lacks the capacity to support the private sector financially.

(-) Vulnerability to leadership change

After the independence from Russia (1991) an authoritarian political regime has been established around president Nazarbayev, which guarantees his policy endlessly. Nazarbayev’s advanced age and rumours about his poor health indicate that a change of leadership is imminent. As the parliament lacks a genuine opposition and there is no clear successor this may threaten Kazakhstan’s stability.

Key developments

1. Economic increase expected to decrease strongly

Kazakhstan is highly dependent on mining industries and in particular on the hydrocarbon sector, which accounts for approximately 60% of total exports and additional than 25% of GDP.

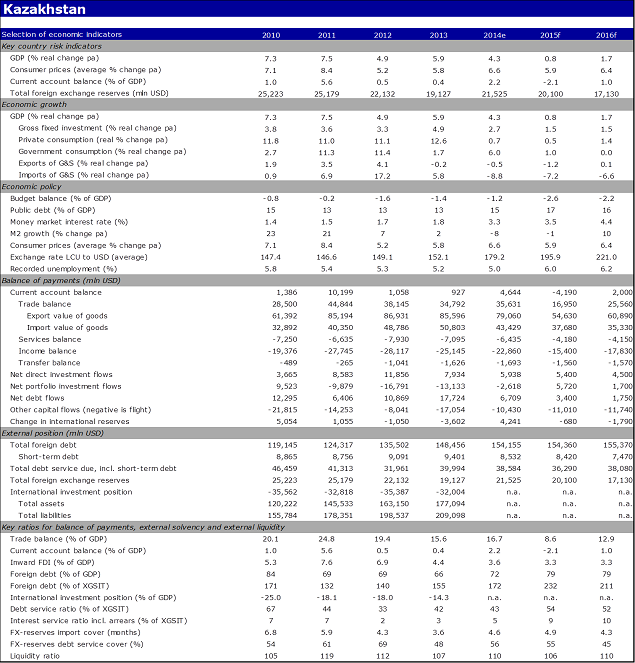

In 2014, real GDP increase slowed markedly to 4.3% from 5.9% in 2013 due to weaker domestic and external request. This came as a consequence of the sharp decrease of the oil price during the second half of last year, the devaluation of the local currency in February 2014 (-19%) and weaker external request from China and Russia for Kazakhstan’s commodity exports. Private consumption, in particular, was hit hard by the negative wealth result resulting from the devaluation, a tightening of lending conditions for consumer loans, and the delayed impact of the slower increase of real wages in 2013. Because of the devaluation, domestic inflation (CPI), increased gradually to 7.4% year-on-year in December 2014, due to higher imported input prices.

The combination of the above mentioned events have had a critical impact on Kazakhstan’s economy. For 2015, the economic increase is expected to fall significantly to 0.8% (e.g. average increase in the previous five years: 6% year on year) on the back of a further weakening of consumption and export increase, resulting in deficits of both the current account and budget balance. It is expected that this situation will only improve if the oil price increases above the fiscal break-even oil price of approximately USD 80 bbl. However, Kazakhstan has shown prudent management of the public finances and reserves accumulated in the National Fund (NFRK) provide sufficient cover for both shortfalls.

Figure 1: Decrease in economic growth

Figure 2: Current account dips into the red

2. A further devaluation of the tenge?

In 2013, Kazakhstan pegged its tenge to a basket of currencies (70% USD, 20% euro, and 10% ruble respectively) in order to smoothen excessive exchange fluctuations. Although the tenge was overvalued, which led to a loss of competitiveness of local industries, the 19% devaluation in February 2014 was not foreseen.

It was the second devaluation in five years (23% in 2009) and once again, it had a critical impact on households, companies and foreign investors. The authorities, however, justified the devaluation as a response to the deterioration in the current account balance, concern about competitiveness due to depreciation of the Russian ruble, and a fall of the central bank’s international reserves. There is still pressure on the tenge, as the ruble depreciated even further next the last tenge devaluation and households and companies are trying to hedge by converting their tenge-savings into USD (about 55% of all deposits are FX-denominated). Meanwhile the central bank is spending billions of its gold and FX-reserves and is closing currency swaps to support the currency. As the decreased oil price generates less USD gain, it makes Kazakhstan additional vulnerable and an extra devaluation may occur.

3. Vulnerable banking sector

Prior to the world financial crisis, Kazakhstan experienced a high and unbalanced increase to large extend fuelled by a credit boom. This resulted in increased foreign deficit and FX-denominated loans. As financial conditions tightened with the onset of the world financial crises, banks lost access to foreign financing and were forced to deleverage aggressively.

Combined with the tenge devaluation in 2009, this led to a significant increase of NPL’s and government intervention was needed to support banks. Although the government aimed at reducing the large stock of NPL’s, e.g. by tax exemptions for write-offs and a Problem Loan Fund, the evolution has been limited so far. At the end of 2014, NPL’s - mainly reflecting loans to corporations and SME’s - still constitute for about 25% of total bank loans. This combined with the large share of FX-denominated loans and savings has made the financial sector vulnerable to external shocks. Currently about 30% of all bank loans and 55% of all savings are FX-denominated. The last is substantially influenced by the tenge devaluation in 2014.

Factsheet of Kazakhstan

Background information

Kazakhstan is the major ex-Soviet Union national and the ninth-major country worldwide, but it is sparsely populated with 17 million inhabitants (13th lowest people density worldwide). The extractive sector, the backbone of the economy, is dominated by international companies, which activities are financed by their foreign parent companies. As a result, Kazakhstan has a high level of private foreign deficit. The national is strongly present in the economy. Its investment holding company, Samruk Kazyna, holds assets totalling 50% of GDP, divided over the oil, gas and financial sectors. The participation in the financial sector is a consequence of a government bail-out next the 2009 crisis, at the same time as the banking sector was overhauled. China is the majority significant business partner for Kazakhstan due to its share in trade and investments (China currently holds 24% of the oil sector).

Kazakhstan gained independence from Russia in 1991 and became a multiparty national in 1993. However, 22 years of constitutional changes have allowed President Nazarbayev to establish an authoritarian political regime that guarantees his policy endlessly. However, his advanced age and rumours about poor health of the president indicate that a change of leadership is imminent. In this regard it is worrisome there is no clear successor. The country’s parliament lacks a genuine opposition and political space has been reduced since 2011, next violent protests triggered the president to step up his repression of dissent. Press freedom is restricted and corruption is persistent. In the long term, Islamic extremism fuelled by socio-economic tensions and a security vacuum in neighbouring Afghanistan could become a problem for the country. Kazakhstan has historically developed strong ties with Russia and joined the Eurasian Economic Union in 2015.

Economic indicators of Kazakhstan

- Kazakhstan News

-

- KAZAKHSTAN: No decision yet on financing production increase at Tengiz oilfield

- KAZAKHSTAN: Kazakh prosecutor's office reports about coup attempt

- KAZAKHSTAN: Kazakhstan reveals grain export volumes

- KAZAKHSTAN: Central Bank sets manat rate for May 25

- KAZAKHSTAN: Kazakh hydrocarbon field's shareholders membership changes

- AFGHANISTAN: Global growth will be disappointing in 2016: IMF's Lagarde

- Trending Articles

-

- KENYA: Kenya's tea industry moves toward strategic diversification

- SOUTH AFRICA: South Africa to extend ICT reach

- GHANA: Ghana steps up to secure electricity supply

- TUNISIA: Tunisia augments ICT exports and connectivity

- GABON: Gabon moves to solve housing deficit

- DJIBOUTI CITY: Djibouti takes steps to overhaul banking sector

.gif?1356023993 "Business Park of Mauritius Ltd, Mauritius")